Financial Wellness and Mental Health: The Two Sides Of The Coin

Understanding Your Money Story: How Your Past Shapes Your Present (and Future) Financial Wellbeing

When it comes to money, one of the things that most don’t tell you about is how it connects to your mental wellness/mindset – like peanut butter and jelly – mustard, and ketchup (if you know the reference points, I clap for you). While this has been true since the beginning of fiat money, responsibilities, and everything costing - it seems like the pandemic put the coin flip of mental health and financial wellness within a constant toss that many are waking up to.

Even though the times have been unprecedented, the flip between the two has been one of the harshest things to witness in my life on repeat. Not only in my wallet but within the mental/currency wallets of others. It’s May, which is Mental Awareness Month, and I wanted to add some thoughts on how this side of the coin can matter to how you view your life - not just the vision of it but also how pockets of value show up. I want to talk about something that goes way beyond numbers: the connection between your financial well-being and your mental health. They are like two sides of the same coin – one impacting the other in surprising ways.

A 2020 study by the National Endowment for Financial Education found that adults with fair or poor mental health are twice as likely to report financial problems (source). There’s been countless articles, think pieces and content around the fact that the coin flip between financial and mental wellness is real but doesn’t connect with how it shows up in the reality of people’s livelihood. I know for me - there have been times when I’ve been through poverty and taken some of those actions/tactics I’ve experienced and applied them in different seasons to do better, but on the other side of my coin - I would be afraid to spend money when I had the abundance. Folks love to say that money can’t buy happiness, and neither does poverty - but the coin flip in this is that your mental wellness during your high tides/low tides with finances shapes your overall perception of your paper/money. Financial anxiety is so real and can have a real impact on not only your accountability but to your accounts.

My Coin Flip -

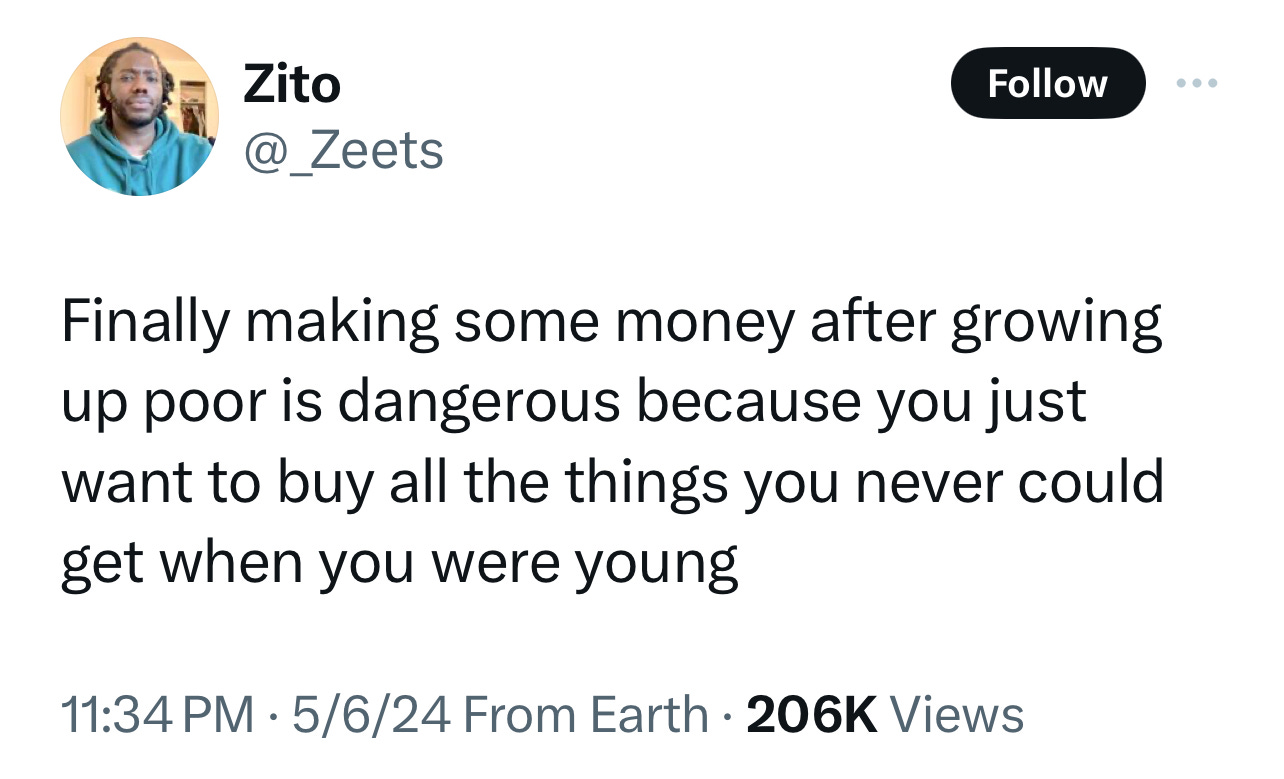

One of my flips dates back to when I was making nearly $10K a month but was scared to buy certain things outside of necessities/bills when I budgeted for them. I thought about this when I saw this tweet about saw a tweet about someone saying they buy things now based upon a season of their coin flip when they didn’t have it. I experienced this as well. A 2021 study published in the Journal of Consumer Psychology found that 82% of participants who engaged in retail therapy to improve their mood later experienced feelings of regret (source).

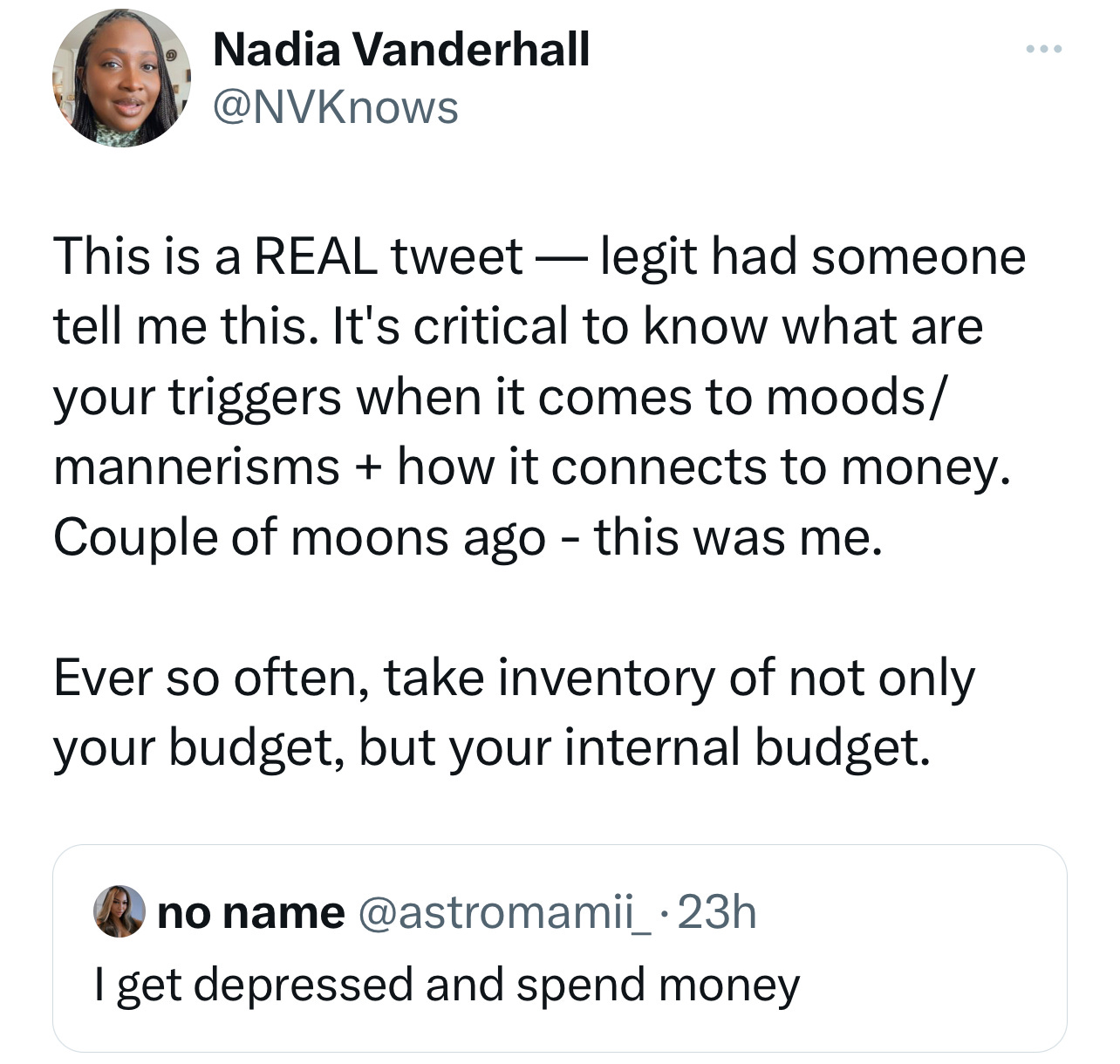

Another tweet I saw was around someone saying that when they are sad, they go shopping/ spending money, etc. Can we say “seen” on this as well? Because it’s true. When I found myself unemployed unexpectedly - I went shopping. I preach to give yourself grace during those tough moments, not swipes.

And when it comes to Financial Planning or personal finance in general, the whole spin that I’ve started adding to my practice is the behavioral finance aspect that goes into how you handle money. So many people are unaware of their origin story when it comes to money and how it layers into where they are with how they make, handle, spend, and grow their money. One client talked about how they would see their parent's budget on the back of an envelope and it clicked for me that I did as well, which pushed me to add that to my content.

Life traumas can’t compound into financial trauma and tactics if we let it. Think of the pandemic, many people were fearful of potentially dying due to COVID-19 and started to overly spend or save due to it. YOLO of it all adding a hiccup to their yielding for the future. Thinking back to your first story with money or even one that triggers you would be a great part for you to journal about and see how it ripples into your money in the current day.

The Money Rollercoaster: Budgeting for Ups and Downs

Life throws us financial curveballs. Sometimes, we're juggling bills, feeling the stress of not having enough. Other times, a raise or a new job might bring a sudden influx of cash. Both situations can be tricky.

Feeling Broke? Budgeting becomes crucial. Track your income and expenses (every cent counts!). Find the balance of needs over wants, and explore ways to cut back (think brown-bag lunches instead of daily takeout). Remember, a budget is a roadmap or a plan for your money–, not a punishment. Adjust it as needed, and don't be afraid to seek free or low-cost financial counseling (like myself).

Suddenly Overwhelmed Or Underwhelmed? Don't fall into a spending spree! This is a chance to build a financial safety net. Consider a sinking fund for things like shopping, invest for the future, and even treat yourself reasonably.

The Shopping Blues: When Spending Makes You Feel Worse

Let's be honest, retail therapy can be tempting, especially when feeling down. But here's the secret: those purchases rarely bring lasting happiness. In fact, for some, spending during depression can worsen the cycle.

Action Step: Acknowledge the emotional trigger. Distract yourself with healthy coping mechanisms – exercise, spending time with loved ones, or a creative hobby. I tweeted some low-spend/no-spend options here a couple of days ago.

Read My Blog! I have a blog post all about the "ADHD Tax" – how forgetfulness or impulsivity can impact finances. The tips here can help anyone who struggles with emotional spending. A 2019 study in the Journal of Attention Disorders suggests that adults with ADHD are twice as likely to experience financial difficulties compared to those without ADHD.

Taking Charge of Your Financial and Mental Wellness

Here's the good news: you have the power to improve both aspects of your well-being!

Financial Self-Care: Make a budget, track your spending, and set savings goals. Feeling financially prepared reduces stress and anxiety. If you feel that you don’t have enough cash to carry a self-care routine - set a tiered system to low cost to splurge that you could use to maintain your coin flip.

Mental Health Matters: Take care of yourself! Prioritize sleep, healthy eating, and exercise. Don't hesitate to seek professional help if needed.

Extra Money: Here are some journal prompts you could start with:

Money Memories And Milestones:

Origin Story: Think back to your earliest memories of money. How did your family talk about it? Did you receive an allowance or have chores with financial rewards? Were there times of abundance or scarcity? Write about these experiences and how they shaped your initial beliefs about money.

Milestones & Turning Points: Jot down significant financial events in your life. This could be your first job, a major purchase, a period of debt, or achieving a savings goal. Reflect on the emotions associated with these milestones and what you learned from them.

Financial Wellness Check-In:

Mental & Financial Harmony: Rate your current financial stress level on a scale of 1 (low) to 10 (high). Then, describe your overall mental well-being. Is there a correlation you notice between the two?

Spending Triggers: Think about recent purchases you made. Were they driven by needs, emotions (boredom, stress, etc.), or social pressures? Identify any emotional spending triggers and brainstorm healthier coping mechanisms.

Remember, you're not alone. By taking these steps, you can create a healthy balance between your financial well-being and your mental health, paving the way for a brighter future.

Question: Do you think that imposture syndrome and lifestyle creep are relatives?